A contingency refers to a condition, situation, or set of circumstances where it is uncertain whether or not a gain or loss will occur in the future. The result of the current condition, situation, or set of circumstances, is unknown until future events occur (or do not occur). Contingencies are different from estimates, even though both involve a level of uncertainty. Calculating depreciation using an estimated useful life or amounts accrued for services received are not contingencies.

A contingency refers to a condition, situation, or set of circumstances where it is uncertain whether or not a gain or loss will occur in the future. The result of the current condition, situation, or set of circumstances, is unknown until future events occur (or do not occur). Contingencies are different from estimates, even though both involve a level of uncertainty. Calculating depreciation using an estimated useful life or amounts accrued for services received are not contingencies.

FASB Accounting Standards Codification (ASC) 450, Contingencies, details the proper accounting treatment for loss contingencies and gain contingencies.

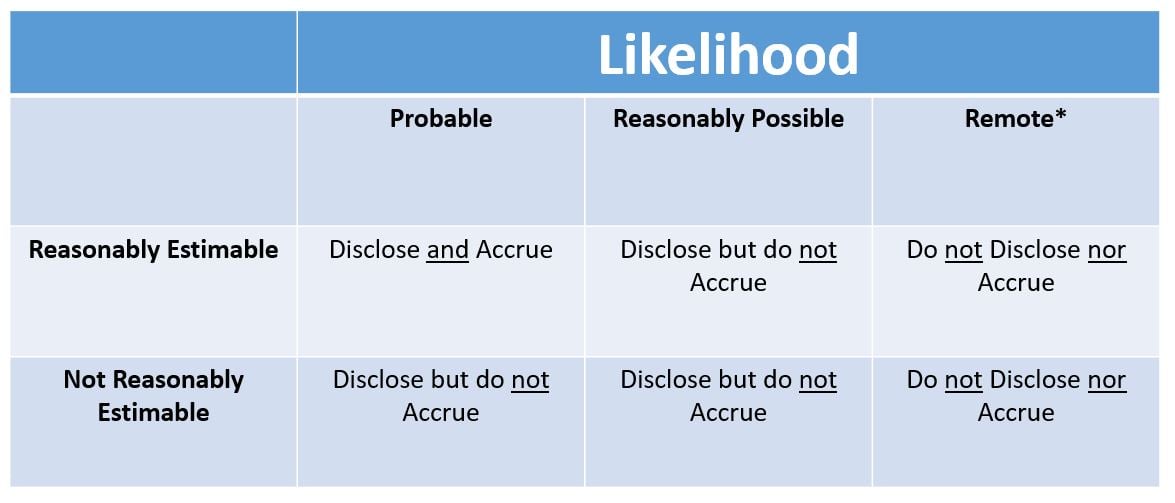

Loss contingencies exist when there is a future possibility of the incurrence of a liability or an asset impairment, and includes pending litigation or potential claims. The proper accounting treatment for loss contingencies is based on two factors: (1) the likelihood of the loss occurring and (2) the ability to estimate the amount of the loss.

The likelihood of the loss occurring falls under three thresholds: “probable,” “reasonably possible,” or “remote.” While FASB ASC 450 does not provide qualitative thresholds for each of these classifications, in practice it is often acceptable to consider probable as over 70%-75%, remote as under 10%, and reasonably possible as anything in between.

The ability to estimate the amount of the loss means being able to reasonably estimate the most likely amount for settlement if the event were to occur. If the most likely amount is unknown, but there is a reasonably estimated range, then it is acceptable to use the range and apply the minimum limit of the range.

The table below can be used to help understand the proper accounting treatment for loss contingencies, based on the two factors above:

* Disclosure of the remote loss contingency may be required – see FASB ASC 450 for further details.

* Disclosure of the remote loss contingency may be required – see FASB ASC 450 for further details.

Gain contingencies exist when there is a future possibility of acquisition of an asset or reduction of a liability. Typical gain contingencies include tax loss carryforwards, probable favorable outcome in pending litigation, and possible refunds from the government in tax disputes. Unlike loss contingencies, gain contingencies should not be accrued as doing so would result in recognizing revenue before it is realized. Disclosure should be made in the financial statements when the probability is high that a gain contingency will be recognized.

Please contact us with any questions you may have regarding contingencies. We are available to discuss and help you determine how to properly account for these situations.